Comparing Historical Municipal Bond Returns to Stock Returns

In this article, we compare municipal bond market returns to the S&P 500 historical market returns from 1991 to 2016. You may be wondering why compare two financial instruments that are as similar as apples and oranges. The reason is simple, one instrument presents less risk and volatility versus the other and by comparing historical returns, it is easier to determine if the extra risk is warranted. Furthermore, if the assumption is that future returns will mimic historical returns, then the analysis could be useful for future decision making at best and teach high level investing concepts at worst.

Municipal Bonds

Before we dive into the comparison, here’s some general information on municipal bonds. Municipal bonds are issued by municipalities such as city governments, state governments, or some other government or agency. What makes municipal bonds unique and attractive is their tax advantaged status. According to federal tax law, qualified municipal bonds are free from federal income tax. If the municipal bond is issued on behalf of a municipality in the state in which you live, most states will treat municipal bond income as state income tax free as well.

Be aware that not all municipal bonds are federally tax free. There are certain municipal bonds that don’t qualify for tax advantaged status. It is important to consult with a municipal bond professional to be assured of their qualifying tax status.

Why is it important when comparing municipal bonds to another investment vehicle for municipal bonds to be federally income tax exempt? If one is investing in a taxable account, then you’d have to get higher return in a taxable investment to equal the tax-free return of a municipal bond. To demonstrate this concept, this municipal bond calculator calculates the tax equivalent return based on a person’s marginal tax rate. This will tell you the rate of return needed in a taxable account to equal the municipal bond return.

S&P 500 Stock Market Index

The S&P 500 stock market index is one of the most popular benchmark stock indexes. It has been known as the S&P 500 since 1957. The S&P index has existed since the mid-1800s, although not in its current form. It currently tracks the performance of 500 of the largest companies on the New York Stock Exchange and NASDAQ Composite.

It’s worth mentioning that the S&P is made up of stocks rather than bonds. What is the difference? Stocks are another term for equity ownership in a company while bonds are a debt instrument where money is lent to a company with the expectation of receiving it paid back in full with interest. In the event that a company enters default, the bondholders are paid back with remaining assets first, and then equity/stockholders. Therefore, bondholders assume less risk.

Lastly, it is important to point out that the S&P historical returns are sometimes measured with dividends accounted for and without dividends accounted for. For purposes of this article we look at the S&P 500 both with and without dividends.

S&P 500 versus Municipal Bonds Risk and Volatility

Why is the S&P 500 so different than municipal bonds? The S&P 500 fluctuates with the value of its underlying holdings and because it assumes more risk, the price fluctuates as the value of the underlying companies change. The value of the underlying companies is generally calculated as a function of the company’s future earnings potential. Because future earnings are much less certain and predictable than the interest payments on a bond, the stock market fluctuates more.

One way to measure this difference in volatility is the standard deviation. The standard deviation is a way to measure how much the rate of return from year to year deviates from the average rate of return. The standard deviation can be calculated on any set of returns to determine its relative volatility to another set of returns. For example, the S&P with dividends, from 1991 to 2016 had a standard deviation of 17.23%. When compared to the standard deviation of 5.35% for municipal bonds during the same time period, you can get the picture that stocks are more than 3 times more volatile than municipal bonds.

What else can be learned from the standard deviation? As we stated earlier, the standard deviation is the expected amount that returns deviate from the average return each year. The S&P 500 with dividends has an average return each year of 11.45% with a standard deviation of 17.23%. This means that one can expect there to be some years with a negative rate of return as the standard deviation of 17.23% below the average rate of return would cause the return to enter negative territory.

On the other hand, the average return of municipal bonds is 6.03% with a standard deviation of 5.35%. This means that when municipal bonds have a less than average return, it’s possible that it will be negative but not likely that it would be extremely negative which is more likely with the S&P 500 index.

Average vs Annualized Returns

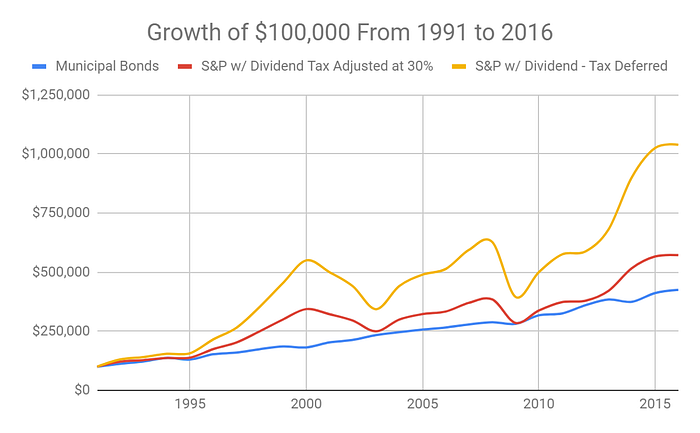

We’ve talked briefly about the average returns of the S&P 500 versus municipal bonds. To revisit those, the average return of the S&P with dividends is 11.45% while municipal bonds averaged 6.03% during the same time period. To rely on the average return to make decisions is misleading. That is because the average return doesn’t consider volatility into its returns. For example, if a person loses 10 percent one year and makes 10 percent back the next year, the average return is 0 percent, but they’re annualized return is still negative. This demonstrates how the average return can be misleading. That said, the annualized return of the S&P 500 with dividends from 1991 to 2016 is 9.90% while the municipal bonds return is 5.9%. That is almost a four percentage point difference over the course of 25 years. At this point, it seems like a no brainer that a person would invest in the S&P over municipal bonds every single time.

Not so fast! In the next section we talk briefly about the relative tax implications.

Do Taxes Really Make a Difference?

Let’s examine an extreme case where an individual is in the top marginal tax bracket of 37% and they are investing in a taxable account. That means that any short-term capital gains they receive from the S&P 500 will be taxed at the 37% income tax rate. If they receive an annualized return of 9.9%, they will have an after-tax return of 9.9% times 63% (100% minus 37%). This equals an after-tax return of 6.23%. So, you can see that this return is not that far from the 5.9% that the municipal bonds offer.

We acknowledge that this example doesn’t account for returns that would be taxed at the long-term capital gains rate or the dividend tax rate which are both lower than 37%. But nor does it account for state and local income taxes which would potentially further eat into the S&P 500’s return.

In Conclusion

It’s worth mentioning that this set of returns is from 1991 to 2016. In the large scheme of things, this 25-year set of returns won’t be like any other set of returns from a 25-year period. It is likely that there will be 25-year returns that are sometimes better than this 25 year and sometimes returns are much worse than these. So, use this at your own risk, however, there are high level concepts that can be learned here.

For example, when accounting for taxes and volatility, it may not be hard to understand why someone would rather invest in municipal bonds over the S&P 500 equity index. This is especially true for someone in or near retirement when taxes and volatility play a bigger role in one’s investment decision making.

Also, from the data and the charts, it is evident that municipal bonds and stock index funds can also serve a complimentary role in an investor’s portfolio. Buying an S&P 500 index fund in a tax deferred or tax advantaged account makes sense to gain faster growth, while buying a municipal bond in a tax advantaged account may not the best idea. However, for investors in the highest tax brackets, who have more to invest than the tax advantaged accounts can allow, municipal bonds can be a great asset class to own inside taxable accounts.

Regardless of one’s decision, we hope this article helps people make more informed decisions so that they can maximize return while minimizing risk over the long term.

About the Author

This article is written by IQ Calculators who strive to create smarter financial calculators for the more discerning financial minds. The owner of IQ Calculators is Brent Hecht who holds an MBA from Texas Christian University.

Like this article? Read More at Value Stock Guide’s Edition on Google News

Originally published at https://valuestockguide.com on May 26, 2019.